.jpg)

2011 proved to be a new record year for the Belgian solar PV market, with over 687 MW of new installations nationwide and an accumulated capacity of 1,669 MW by the end of the year. This growth can primarily be related to the Flanders region, accounting for 86% of the growth in capacity, but has also taken shape in Wallonia (<14%) and Brussels (<0.2%).

Flanders (86% of the Year’s Growth Belgium)

In contrast to fears that the PV market in Belgium would be negatively impacted by a series of green certificate value digressions in Flanders, the year saw the installation of a large number of PV modules. Volumes recorded by VREG rose fast, with a preliminary record of 163.4 MW for installations larger than 10 kW in June, just prior to the July 1 digression (certificate value becoming €300/MWh, installations >250 kW €240). VREG reported a near record number of 6,410 requests for small installations that were almost immediately approved in that month.

Registered residential capacity grew considerably, in particular in the second half of 2011. On average, over 7,700 new installations (max. 10 kW) per month were recorded during that period, with an average new volume of over 39 MW/month. The share of this market segment increased in total volume from 45% (2010) to 64% (2011).

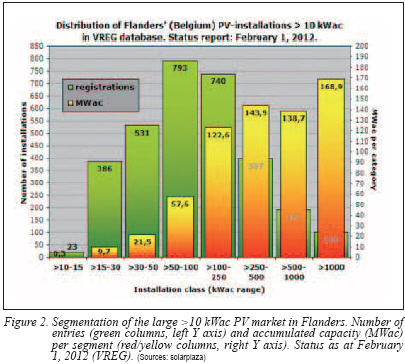

A preliminary 2011 record volume of 592.3 MW new capacity was registered by VREG in their last update, including 76,508 new entries, with 208 over 250 kW. That is 76% over the adjusted volume for 2009 (454.2 MW). Market segmentation was 379.0 MW up to 10 kW (system average app. 5 kW/installation), 65.0 MW entries between 10 and 250 kW (11%), and 146.3 MW for the largest installations of above 250 kW (25%). For the latter two categories, 660 and 208 new entries were recorded in 2011 (entries may be segments of larger projects). The biggest new projects recorded were the 4.1 MW ‘solar tunnel’ above the high-speed train track northeast of Antwerp; a 4.5 MW/36 hectare ‘solar parking’ at Hodlmayr’s in Tongeren; and The Benelux’s largest project, a 6.2 MW free-field installation at Nyrstar in Overpelt. ING Equipment Lease’s portfolio grew rapidly in 2011, now accumulating 66 MW, with 166 projects (mostly large) sized 20-3,239 kW. The Antwerp region east of the River Schelde has also seen some new large projects. Katoen Natie’s Loghidden City terminal (Schelde West Bank) remained the biggest single-site installation in The Benelux (27.9 MW).

VREG updates in 2011 revealed a 170 MW ‘backlog’ volume increase for 2010 since February 2011. It is, therefore, expected that much more capacity will be added to last year’s volume, possibly reaching 750 MW in 2011, or more.

.jpg)

Wallonia (<14%)

CWaPE reported strong growth in Wallonia, doubling from 83.3 MW, cumulated from 21,233 installations of max. 10 kW, originally reported at the end of 2010 to 181.6 MW and 40,181 installations at the end of 2011 (growth without corrections: 97.8 MW). At the end of January 2012, 90 installations larger than 10 kW were recorded, with a capacity of 6.5 MW (share 3.3% of total accumulation; average 72 kW/installation), which is increase of only 4.4 MW (47 installations) since the end of 2010. Two new installations were implemented in Ghlin and Strepy-Bracquegnies, with a maximum size of 250 kW. Actual calendar year growth volume is not yet known. Apere estimated a year growth volume of 94 MW and 186 MW accumulation based on the status as at end September that year.

Brussels (<0.2%)

The last available data for Brussels (September 2011) shows a meager growth of only 819 kW (169 new installations) and an accumulated volume of 6.7 MW (2,041 installations) as compared to data shown in the year 2010 report (accumulation 5.9 MW, 1,872 installations). Apere estimated a yearly growth of only 1.1 MW, accumulating volume to 7.0 MW in 2011. Two new larger projects will change that only a slightly: 150 kWp on Plastoria’s roof (realized end of 2011), and a planned 1.6 MW project on the TIR center.

Belgium

According to present data, Belgium had accumulated 1,669 MW end of 2011, with shares larger than 88% for Flanders, over 11% for Wallonia, and 0.4% for Brussels─ with more volume yet to be added. Taking a conservative ratio (DC:AC=1.1:1), 1,836 MWp PV generator capacity could already have accumulated. Thus, an average 167 Wp PV module could have been installed for each of Belgium’s 11 million inhabitants (EU27 average 2010: 59 Wp).

In 2010, 595 GWh of solar electricity was generated in Flanders, while a preliminary 1.2 TWh has been registered for 2011. During the freezing mid-winter conditions, as at January 27, 2012, between 4 and 8% of Belgium’s electricity consumption was covered by photovoltaic conversion of sunlight during the day.

Although green certificate value for PV projects larger than 250 kW has now dwindled to 90 euros in Flanders, and large projects seem to have come to a standstill, the residential and commercial sector still look promising, with low module prices. How much volume that will generate in the crisis year 2012 is hard to predict.

*MW = MWac (inverter capacity, hence not referring to module capacity)

** Status in this article based on February 1 and February 6, 2012 reports by VREG, and January 2012 reports by CWaPE, Apere (Sources: Apere, BRUGEL, CWaPE, EurObserv’ER, PV-Vlaanderen, VREG)

Further Information: solarplaza (www.thesolarfuture.be)

For more information, please send your e-mails to pved@infothe.com.

ⓒ2011 www.interpv.net All rights reserved.

|

.jpg)